Multipolarity Brief: Issue 14 — Iran Special IX

Strangling the Dragon: Myth BUSTED

Since Trump ordered the US Navy to blockade the Persian Gulf, an old narrative has started taking hold again. It often seems to go unanswered. It even gets traction among otherwise intelligent people who should know better. It is increasingly a line of argument used by Trump loyalists on social media. But it does not stand up to scrutiny. It is therefore time to sound the horn, push down the plunger, and blow up once and for all one of the big ‘theories’ about Washington’s motivation for the Iran War: that it is really, secretly aimed at China. Once again, the Multipolarity Brief will be doing the job the legacy media often doesn’t and getting you, dear readers, well ahead of the 8-ball. Giddy-up!

On Sunday, an X (formerly Twitter) user replied to a post by Multipolarity co-host Andy Collingwood on this matter. He wrote:

We don't want the strait open. None of the tankers are heading to America. Go get a copy of Sun Tzu. We are… Exposing the weakness of the Chinese; how easy it is to blockade their energy and food imports... This is little more than a training exercise for our Navy. And like a castle siege, time is on our side.

We share this not to single him out. And we have not linked to the original, because we do not want a pile on. We share it because it encapsulates in tone and content a theory that has gained traction among Trump loyalists since the beginning of the conflict — and has enjoyed a resurgence since the blockade was announced.

Jack Prosobiec, a veteran of US Naval Intelligence, and now a prominent pro-Trump influencer with more than three million X.com followers, wrote on 13 April that “The oil from Iran goes to China. You put pressure on that, you're cutting off one of the arteries of the dragon.” On the 15 April, he was even more stark:

Mr Prosobiec is one of many. The theory is spreading and popular.

Let us be clear: this is almost certainly not Washington’s reasoning for the blockade specifically, or the war in general. If it is the secret motivation, then it is colossally stupid.

Fully eight weeks ago, at the beginning of this war, Multipolarity Brief explained why the ‘China-as-the-real-target’ argument did not bear much consideration. We showed that since the end of the Second World War, the US had made it perfectly clear in its actions that it would not accept a government in Tehran that was not explicitly pro-Western (or, more to the point, pro-US). It supported a coup d’etat in 1953 to overthrow Mohammad Mossadegh and replace him with a US puppet. It ferociously opposed the Iranian revolutionary state, which replaced the pro-US Shah, including supporting wars of aggression against Iran and imposing a swingeing regime of sanctions. China never entered the conversation before, so it seemed strange to believe it is the ‘true’ target this time. (Read in full detail here.)

Yet there is an equally important point to be made about this line of argument, especially as it pertains to the blockade: China is nowhere near as vulnerable as supposed.

The top line numbers are seductive, of course.

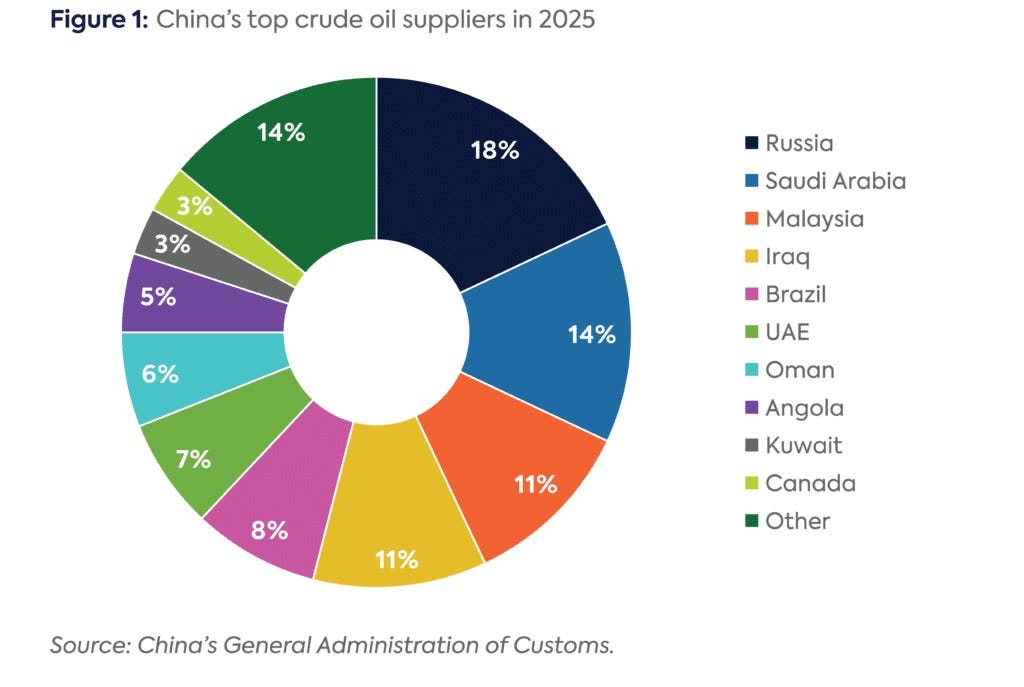

China imports 70-73% of its crude oil, with total seaborne crude imports averaging 11.0-11.5 million barrels per day in recent years. In 2025, 40-50% of those crude imports originated in the Middle East (Saudi Arabia 14%, Iraq 11% and Iran, unofficially via rebranded barrels, 11-12%). Roughly 45-50% of total crude imports (or some 35% of overall crude supply when including domestic production) transited the Strait of Hormuz.

Given China consumes more energy than the US and EU combined — and the amount it consumes is rapidly growing — does it not stand to reason that the blockade of the Strait will be a disaster for the Chinese economy?

No. Or at least not in relative terms.

First, China has significantly diversified its sources of crude imports. Russia has been China’s leading supplier for years (~20% of imports), with a growing share via the ESPO pipeline (hundreds of thousands of barrels capacity, bypassing sea chokepoints entirely) and Pacific routes. Russia could no doubt be relied upon to ramp up exports to China even further, given how close Moscow has drawn to Beijing since 2022. Other non-Hormuz sources have risen to 57% of China’s imports of crude, recent data show. The Middle East share of oil imports dropped to 42% by 2025. Meanwhile, direct pipelines from Central Asia, Russia, and Myanmar help insulate the country from sea-lane risks.

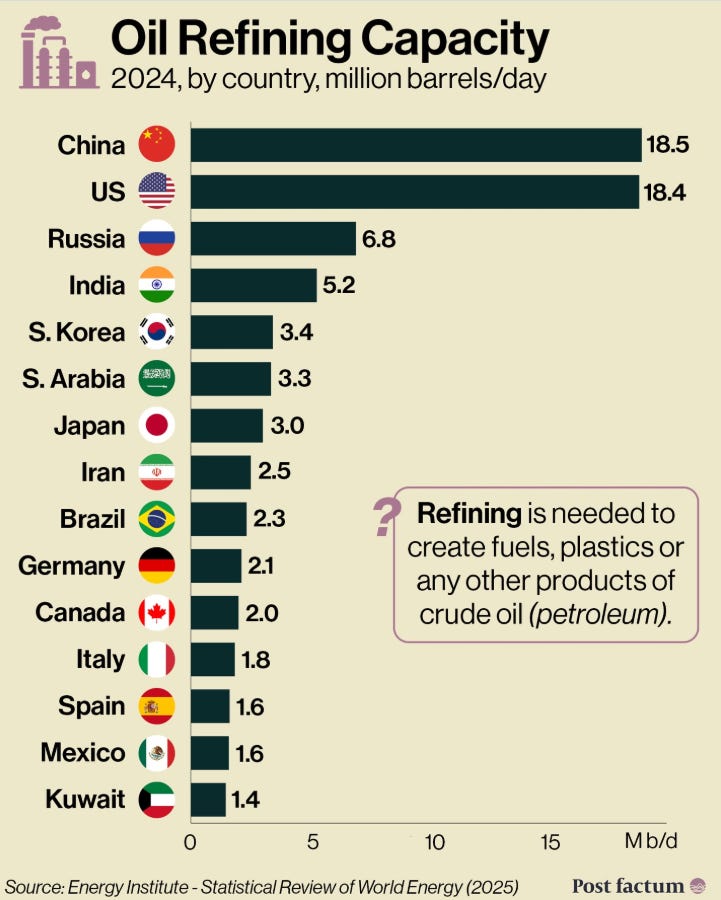

Secondly, China is the world’s largest refiner of crude oil, and is a major net exporter of diesel, gasoline, jet fuel, and fertilisers. When the Strait of Hormuz was first shut down, Beijing moved quickly to impose bans or curbs on refined fuel exports, which started on 4 March. Fertiliser exports faced similar controls or outright suspensions a little later. China’s refineries normally export the equivalent of 1-2 million barrels of oil a day of oil products. By trapping that output within the country, Beijing reduces the crude-oil volumes it needs to import to refine. One signal of how this is working is that domestic diesel prices have decoupled from the global spike, moving downward even as the rest of the world suffers the pain of price increases.

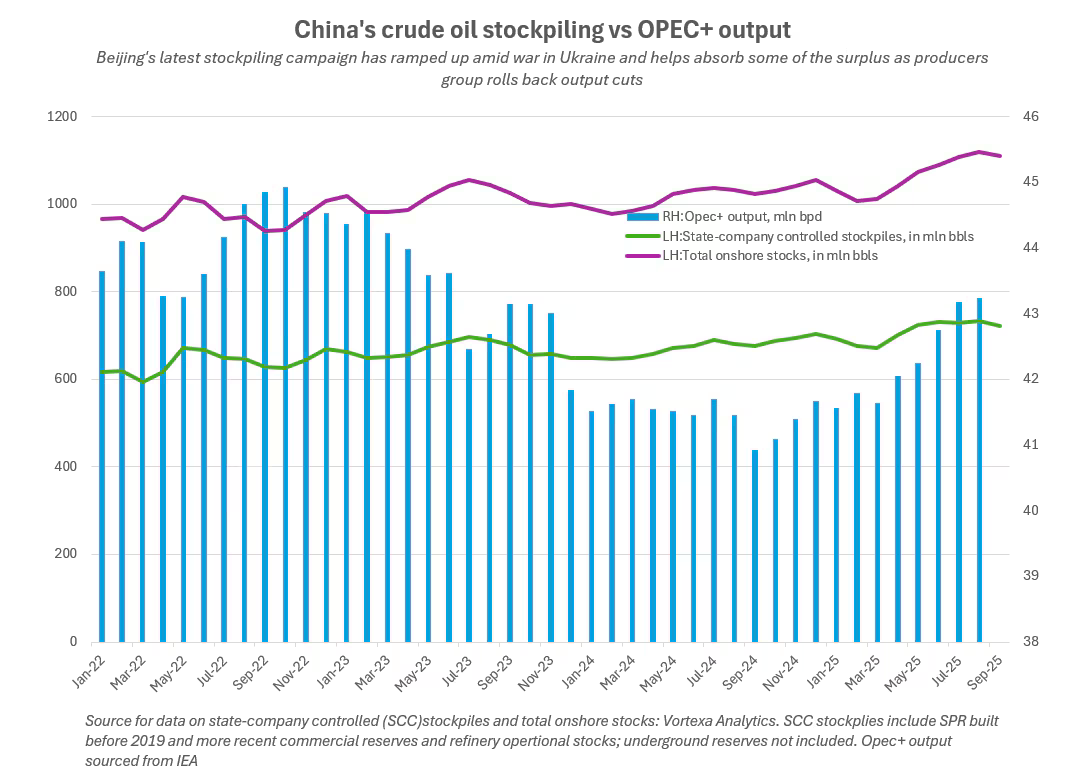

Thirdly, Beijing has built enormous stockpiles of crude oil. It entered this crisis with some 1.4 billion barrels in combined strategic petroleum reserves (the government holds some 360 million barrels, while commercial stocks are approximately 1 billion barrels). This covers ~120 days of total net crude imports at 2025 levels. We must note on this number that it means the country’s reserves cover three months of total crude imports. In this crisis, only the Hormuz-specific volumes are cut off. Various media and industry estimates put the coverage of a total Hormuz cut off at about seven months. So, even if every last barrel of oil from the Gulf had been cut off since the beginning of March (something we know not to be true, given some Iranian shipments were still flowing well after the Strait was 'shut’ for just about everybody else), and China failed to compensate this loss through the purchase of extra from elsewhere (also unlikely, as we shall see below), the China’s reserves would still last well into September.

Fourthly, as big as China’s oil reserves are, its pile of currency reserves are even bigger. Massive. Gargantuan. Yuuuge. China has a giant currency reserve. Estimates place it at over $3.3 trillion. This is more than enough to outbid competitors for oil on the spot market and suck in whatever crude is available — at almost any price — for months or even years.

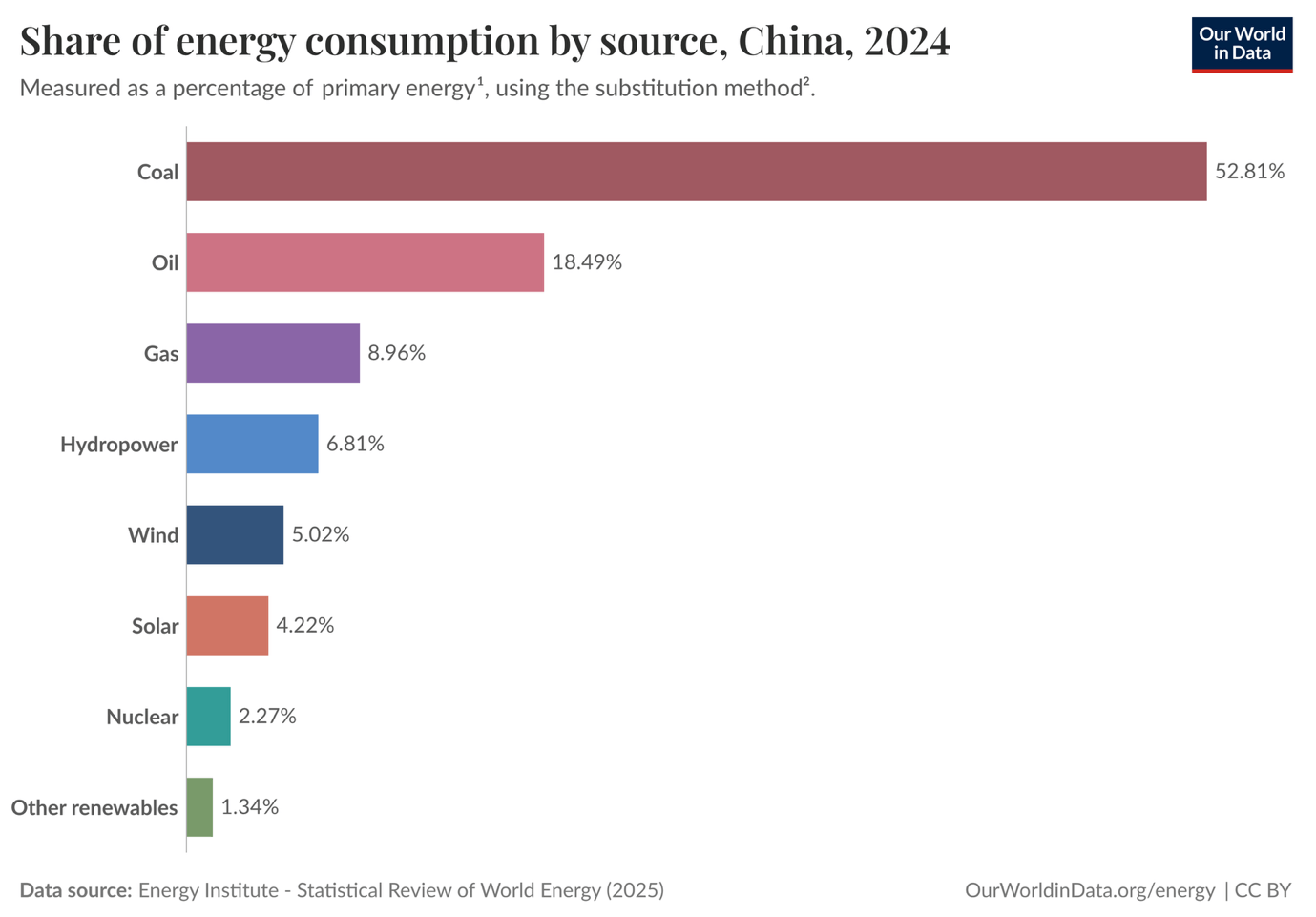

Fifthly, oil is not even the largest part of China’s energy consumption: that comes from coal, at 53% (chart, below). Oil is a far smaller proportion, at only 18.5%. Of that, 30% is domestic production. Hormuz, as we have seen, accounts for only 42% of China’s oil imports. Thus, the amount cut off is a little less than 6% of China’s overall energy consumption. This is far lower proportion of China’s primary energy consumption than come from renewables, which account for 18%.

This combination of coal and renewables makes the Chinese grid uniquely insulated from the shock. In 2025 alone, Beijing added some 315 GW of solar capacity and 119-120 GW of wind — more new renewable capacity than the rest of the world combined in recent years. For context, global wind additions hit a record 165 GW in 2025; China took 73% of it.

How much of China’s energy production could it re-direct away from oil and gas toward other sources? And how much electricity does China have to spare? The AI and Data Centre situation offers a clue: while it is becoming an increasing bottleneck in the United States, Beijing has built out enough cheap, dispatchable power (coal + renewables + nuclear) to the extent that data centres are projected to take only 2-3% of total Chinese electricity by 2030, versus some 7% in the US.

The primary energy use of oil in the Chinese economy is ultimately logistics and transportation. Yet here again, Beijing is far ahead of the curve, dominating in the EV and battery production industry (note well, not leading: dominating). EVs now account for some 50% of new car sales in China, which is the largest EV market in the world by far.

Fifthly, China’s economy is in deflation or lowflation. While inflation from an exogenous shock would be far from ideal, the current deflationary environment does give the People’s Bank of China room to mitigate the blow from a Hormuz-induced economic slowdown. Interest rates on China’s sovereign bonds have traded in a band between 1.70% and 1.85%, far below their US and European counterparts. The West could be caught between a Scylla of easing monetary policy to cushion the economic downturn and a Charybdis of tightening monetary policy to curb inflation. Less of an issue for China.

Finally, although China is no longer a Marxist-Maoist economy, it retains control over the economic levers and prices in a way that the west does not. The central government sets retail fuel and electricity prices directly (via the NDRC mechanism). It has repeatedly capped or delayed full pass-through of international crude spikes (e.g., limiting March/April hikes to roughly half the formula). This insulates households, logistics, and industry from immediate pain. As we have seen, the government has been able to rapidly impose export controls. It has also invested in coal-to-liquids/chemicals technology that could be rushed ahead. It could probably impose curbs on the sale of new internal combustion engine vehicles and subsidise EVs, which China produces in such quantities that the country’s commercial competitors in Europe and North America complain of dumping and overcapacity.

Too long; didn’t read? China is nowhere near as vulnerable as you think, bro.

This is not to argue that China’s economy will be unaffected. Of course it will. Not least by the fact it is export driven, and if the world falls into a serious economic downturn, China’s export markets will have less money to spend. Yet this is a far cry from the argument being made by the Trump loyalists and the more dimwitted reaches of the geopolitical analysis crowd: namely, that the US Navy’s blockade of Hormuz will have a calamitous effect on China’s economy through the crude oil and natural gas channels.

In fact, per recent translations provided by the invaluable Sinification, China sees a series of significant economic opportunities. While recognising the threat of higher and volatile energy prices, and to the country’s export markets, some of China’s analysts believe the Hormuz crisis could improve China’s overall manufacturing competitiveness relative to its rivals. They also believe it could generate a renewed clamour for renewable energy, batteries and EVs, sectors in which China is, as aforementioned, dominant. Beijing apparently also sees the possibility to “reroute capital, energy flows and supply chains in Beijing’s favour.” (This, of course, ignores the manyfold strategic benefits; however, this Brief will focus on economic matters.)

Ultimately, China’s elites have been thinking about this scenario for a long time. Decades. They are acutely aware than Washington’s oil blockade on Imperial Japan backed it into a corner from which it had to choose between complete geostrategic defeat and a suicidal pre-emptive attack on the United States. They also study the less well known (in the West) blockade of the newly founded People’s Republic of China from 1949 through the 1950s, which embargoed a number of strategic goods and caused much privation.

As far back as 2003, then-President Hu Jintao publicly warned of China’s “Malacca Dilemma” — the fear that “certain powers” (pointedly the US Navy) could interdict oil tankers in the narrow Strait of Malacca (and by extension Hormuz or other chokepoints) during a crisis. At the time, 75-80% of China’s imported oil passed through Malacca; the strait was seen as a single point of failure. Since then, the Chinese leadership has undertaken a programme — many aspects of which were discussed above — to build stockpiles, diversify imports, move away from oil as a source of primary energy, and protect its shipping lanes in the near abroad. Chinese leadership has wargamed this scenario. They have planned for it over decades. The system is incomplete, but they are as ready as any nation. If Washington wanted to cut off one of the artieries of the dragon, in the words of Mr Prosobiec, it’s probably too late — much like many of the strategic ideas circulating for how America can bring low the Chinese economy.

Yet in the same way that many people still seem to believe the Chinese economy is based on the low wage, mass production of tat for Walmart, and intellectual property theft, so many people still appear to believe that China is as acutely vulnerable to a blockade of Hormuz (or Malacca) as it was in 2003. Old strategies die hard, it seems.

Meanwhile, every minute that the Strait is closed is another minute the world goes without adequate oil and natural gas and aluminium and fertilizer, and ultimately food, clothing, transport, metals, and plastics. The blockade is a long fuse, lit like in the Mission Impossible title sequence, the flame getting ever closer to the point at which it detonates the bomb of global economic catastrophe. At that point: Chinese, European, American… we’re all doomed. No exceptions. No mulligans.

Until the Clouds Roll in a Little…

Did you think the effort we put into researching and writing this dispatch brought you some value? Then take 10 seconds to subscribe right now. Soon, more articles will start appearing here every week. We are tremendously excited about our plans — which are rather ambitious. If you want, you can get ahead of that with a paid sub right now. You will get our premium podcast episodes as part of that. If you truly cannot spare the price of two pints of beer in a pub, could we ask a favour? Take just one minute of your time to share this with somebody who would benefit from reading it. Oh, and if you like a killer deal, for only eight bucks you can subscribe to Multipolarity the Podcast on Patreon. In return, you’d get all our premium podcast episodes, including the back catalogue (in which there are some absolute gems). Knockout deal!

Multipolarity Brief will return next Tuesday. Until then, farewell and good luck.

Other reason a US blockade of China has long been a non starter is that the US is so utterly dependent on imports from China and Taiwan too. The lesson of the current Iran war is that near offshore is not defensible whatsoever. USN would be unable to even approach Taiwan in the event of a showdown, and US economy would rapidly implode from lack of all basic goods and parts. Not least, Trump already tried a trade showdown with the moronic "liberation day" and couldn't even sustain a tariff campaign, so it should be clear a deeper trade cutoff has no viability.

Sorry but I`m not convinced by these arguments. It`s all about China.

This hemisphere of the middle east and south Asia is today what Europe was during the cold war, the centre of the hegemonic struggle of the two super powers, the Sowjetunion back then and China today. Iran sits at the centre of this hemisphere. Bringing Iran back under its influence (if not by regime change by some other kind of dependency) would be a huge geostrategic win for the US.

And on the ecomomic argument. All those points may be true and there is no question that China prepared for many years for these kinds of scenarios. But when it comes to who suffers more pain overall the US as an exporter of oil and gas is in a far better position than China as an importer. No matter how well you prepare, owning the product gives you superior power.