Multipolarity Brief: Issue 12 — Iran Special VII

Blockhead Blockade; Crude Thinking; I-ran into China

Blockhead Blockade

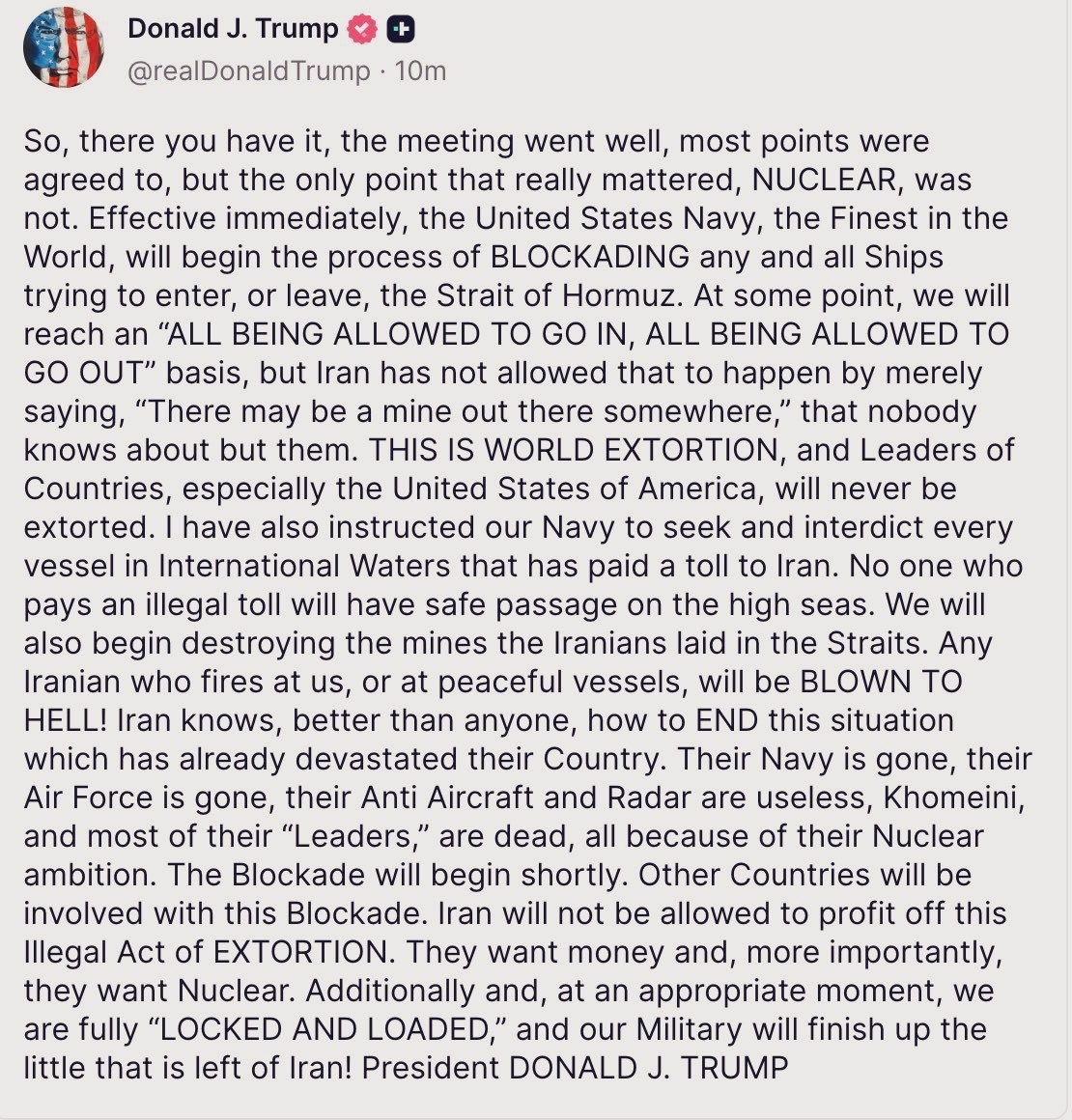

On Saturday, US Vice President J.D. Vance ended negotiations with Iran in Islamabad, Pakistan. The two sides, he said, had not been able to reach an agreement on a permanent peace. On Sunday, US President Donald Trump announced that the US Navy would blockade the Strait of Hormuz: if the Strait wasn’t open to all shipping, it was no longer going to be open to Iranian ships or to those countries that had done side deals with Iran (usually involving large payments in cryptocurrency or Yuan to Iran) either. President Trump called Iran’s position “WORLD EXTORTION”

In concrete terms, how does such a blockade work? The first thing to understand is that as the US Navy cannot enter the Strait, or get anywhere close to it, for fear of Iranian anti-ship missiles (which is why they cannot directly ‘force’ the Strait). Therefore, the US Navy will be stationed farther back, far beyond the Gulf of Oman, in the Arabian Sea, likely in a ring from Oman to India. If the blockade operates as blockades usually do, ships leaving or heading toward the Strait will be ordered over radio to change course. Those which do not follow orders will be either turned back or escorted to a port acceptable to the US Navy. This process can go as far as US Marines and forcing entry to bridges and engine rooms. It is unlikely that the US would start firing on ships refusing to turn — although that is ultimately possible, too.

Let us talk in plain terms. If the aim of this blockade is to extract concessions from Iran in negotiations, or to outright defeat Iran, it is a stupid idea. Not ‘unlikely to succeed’ or ‘questionable’: stupid. Boneheaded. Moronic.

More than a month ago, the Multipolarity Brief explained in a widely shared dispatch that Iran’s strategic aim was to inflict enough pain on the US to make it stop attacking Iran. To this end, Tehran primarily followed a countervalue battleplan. Countervalue means to attack things of value to the enemy, but not necessarily its military. Tehran’s main countervalue tool was the closure of the Strait of Hormuz. This allowed it to cut off the flow of oil from the Gulf region — interdicting some 20% of global oil supplies, including certain heavy grades of crude that are crucial for the world economy (and, indeed, American refineries). In the same way that the EU and US sanctioned Russia for its invasion of Ukraine, hoping to damage Russia’s economy sufficiently that the pain would cause President of Russia Vladimir Putin to cry mercy, so the Iranians were hoping that the economic pain caused by their ‘sanctions’ (the closure of Hormuz) would cause the US and Israel to stop.

It is true, of course, that Iran itself would suffer from its own plan to cut off oil. Before the war, it had to sell its oil at heavy discounts because of sanctions, but it was still generating an income from sales — mostly to China. Now they would likely lose this income.

Nevertheless, the US and Israel were clear in no uncertain terms from the start: they intended to destroy the governing elite in Iran, create a new system of governance, and install a government that would do what Washington said. President Trump even said so when he announced the war on 28 February. Furthermore, the implication was that neither party would be too disappointed if the Iranian state itself ended up being dissolved into warring ethnic statelets and power groups, similar to the Yinon Plan. There is no economic pain Iran could suffer that would be worse than regime change or state dissolution. Therefore, Iran had — and still has — much higher pain tolerance than the US; the balance of resolve is very much in Tehran’s favour, and still is.

Iran understood this well, and this is why it followed a countervalue battleplan centred on interdicting the flow of hydrocarbons from the Gulf: it would feel pain, but the rest of the world could not tolerate nearly as much pain as Iran in this circumstance. Recall that at some level Washington understood this, too: it was allowing some oil out of the Strait, including Iranian oil, because it wished to minimise the effect of the war on the price of oil, and thus minimise the economic pain caused.

And so of course, the sensible thing to do is blockade the entire Strait! To do Iran’s job for it! Great job!

Crude Thinking

Many of President Trump’s supporters are arguing that the blockade will accelerate Iran’s economic collapse. Indeed, Multipolarity has heard several times in recent days that Iran cannot pay its soldiers already. It should be noted, however, that the story about problems with military wages first came from the Jerusalem Post, an Israeli newspaper, about a month ago. It claimed that an attack on a data centre run by Bank Sepah, the bank apparently responsible for Iran’s military and IRGC salaries, had disrupted the payment of wages. More recent stories appear to have originated from Iran International, a Saudi-funded media group that a Guardian investigation found to be “part and parcel of the Saudi crown prince’s decision to take a more aggressive posture against Iran.”

Until evidence emerges from less biased sources that morale among Iranian soldiers and security personnel is declining due to wage payment delays, Multipolarity will continue to view arguments that the blockade is going to facilitate Iran’s collapse as wishful thinking. Iran’s economy is no doubt in a bad state, and has been for years. Nevertheless, in an existential war of regime/national survival, it has a significantly higher pain tolerance than the rest of the world. And it remains true that the rest of the world is heading toward a Great Depression-scale economic calamity. As this Brief explained more than a month ago, the closure of the Strait of Hormuz affects many sectors more or less simultaneously: this is not just going to mean higher energy costs (bad as that would be).

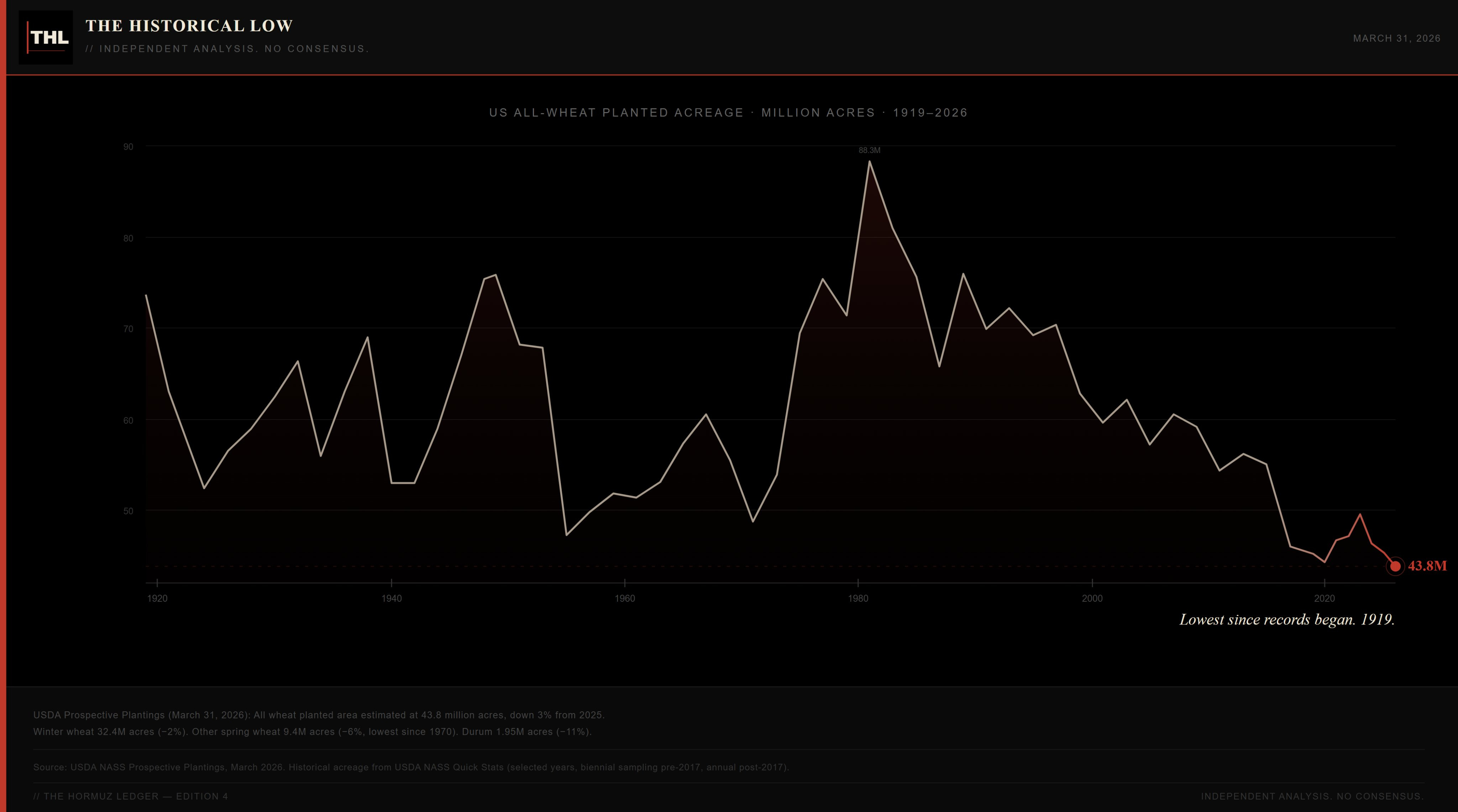

Natural gas is a key feedstock for fertiliser. This means higher fertiliser prices, and thus less fertiliser applied to crops. This means lower crop yields, and thus higher food prices six months or a year hence. This is already happening. The US Department of Agriculture reported that this year the planted acreage of wheat in the US was the lowest since records began (chart, below), even lower than during the Great Depression and Dust Bowl. There are no mulligans for crop planting. If the Strait reopened tomorrow and fertiliser prices somehow declined instantly to norms, it would still be too late for this round of crops.

US all wheat planted area: 43.8 million acres, the lowest since records began

Petrochemicals (those created from crude oil) are the basis for making polypropylene, a versatile, lightweight, and durable thermoplastic polymer that is widely used for packaging, automotive parts, textiles, and medical devices due to its high chemical resistance, fatigue resistance, and heat tolerance. Higher prices polypropylene would increase costs for food packaging and hospitals, and perhaps even lead to shortages.

Petrochemical feedstocks are also the basis of the polyester manufacturing chain. Polyester is the most important material in the modern apparel industry. Factories become unviable with significantly higher polyester prices. Fewer factories operating with much higher input costs mean much higher clothing prices.

Sulfuric acid is vital in the production of copper (the most important metal for electricity grids) and cobalt (an important component of lithium-ion batteries). Sulfuric acid comes mainly from sour grades of crude. A large amount is made in the Gulf and shipped through the Strait, or is made elsewhere in the world from but from sour grades of crude from the Gulf. Disruption ultimately leads to higher grid and battery costs.

The caustic soda and chlorine needed for water treatment, the paper and cardboard industry, and the creation of PVC (used in piping, flooring, cable insulation and window frames) is based on salt and electricity. The process that makes the tyres for vans, trucks and lorries starts with petrochemicals. Higher tyre costs or shortages lead to logistics disruptions and higher retail costs.

The manufacturing process for the glass used in windows, vehicle windscreens and solar panels requires natural gas (remember that glass manufacturers were among the first companies to go to the wall when Europe sanctioned Russian gas). Helium is meanwhile of paramount importance in the production of semiconductors and fibre optics.

Large amounts of electricity are required to refine aluminium. Furthermore, about 10% of the world’s supply comes from the Gulf. Aluminium prices on the benchmark London Metals Exchange have increased from $2,892/t on 27 February to $3,626/t today.

And, yes, oil and gas are also crucial for electricity bills and travel costs, and therefore filter into every part of the economy.

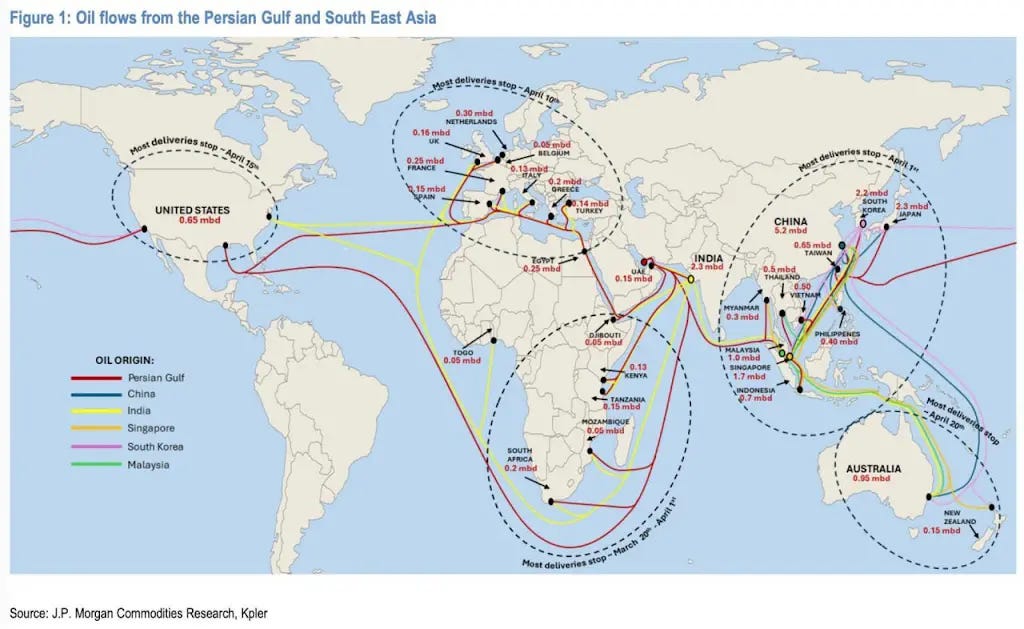

Importantly, as the Multipolarity Brief explained three weeks ago, the ships that were leaving the Strait while it was still open in the early moments of the war are only just arriving at their North American and European destination ports.

The last oil from the Persian Gulf reaches different regions at different times. Europe was last week; North America is this week. (Source: JP Morgan)

In other words, as we wrote at the time, we are only now reaching the point where the economic “effects transfer from Wall Street and the financial world to Main Street and the real world.” Until now, higher prices were confined to the futures market. Now, it is all about physical delivery, which is why the price of dated Brent (for delivery) is so much higher than the futures market price: they have decoupled as buyers scramble to get what they can.

The price of Brent (a benchmark blend of crude oil) futures (a derivative contract) usually mirror the price of Dated Brent (that for physical delivery). Near the end of March, the prices decoupled. Could that be because the US Treasury is buying futures contracts to push the price lower, and thus soften the oil price blow? Either way, the real cost of oil is now much higher than suggested by the futures market——more than 30% higher when this chart was captured in the last couple of days.

The narrative at present seems to be that the collapse of the supply chains in all these sectors will be ‘stagflationary’ (type stagflationary and Iran into Google and look at all the headlines). But a bout of inflation combined with zero economic growth hugely underplays the risks. Instead, the risk is a massive economic contraction plus inflation. Furthermore, the cause — the total disruption of just one node of the globalised economic network shattering everybody’s economy simultaneously — would be likely to prompt a forced re-wiring of the postwar economic system, likely under the pressure of large standards of living declines and social unrest (which has already started in the Republic of Ireland). The scale of the potential economic and socio-political shock has not yet been apprehended by elites or politicians.

I-ran into China

There is another reason that a blockade is a foolish decision: it risks confrontation with China. Beijing had conducted an agreement with Iran and had been receiving oil from the Gulf. Blockading the Strait means blockading Chinese ships. Friend of the podcast Anusar Farooqui (AKA Policy Tensor) was the first to highlight the possibility a blockade would cause Sino-American confrontation. Wisely, he was swift to make the point that shipping and foreign navies were central to the imposition of what China refers to as the Century of Humiliation, during which the Royal Navy, US Navy and Imperial Japanese Navy used gunboat diplomacy, forced port entries and defeated the Chinese at sea. These sorts of idiosyncratic matters are of far more importance than they might seem in anticipating the way states respond to a given action.

The Nemesis Steamer Destroying Chinese War Junks in Canton River, 1843, Edward Duncan

While it seems unlikely that China would put itself up against the US Navy in the Arabian Sea — a battleground on which the US would certainly hold the advantage — it has a range of means to respond and escalate if the US interferes shipping between the Gulf and China. These could range from trade restrictions (recall that China won the trade war it won last year, forcing Mr Trump to back down) all the way up to a blockade of Taiwan. The fact the administration has opened itself up to conflict on a second front while it is struggling to deal with Iran, and coercion from the world’s preeminent manufacturing power while it is about to start struggling against an economic downturn, would seem to be foolish in and of itself.

So, if the blockade is such a stupid decision, why might it have been taken? The most parsimonious explanation is that President Donald Trump and his team are extremely frustrated and so are both not thinking straight and are willing to try anything to get themselves out of the trap they jumped into. As we explained last week, the US has suffered an outright military defeat against Iran, failing to score a single operational victory. It apparently has no military means to stop Iran attacking US allies within the region or to open the Strait of Hormuz. That is why Donald Trump asked for a ceasefire and peace negotiations. That is why he agreed to make Iran’s 10-point plan the basis of those negotiations in order to get Iran to send a team to Islamabad. But now reality sets in: Iran’s asking price is politically unpalatable. Yet the US does not have the military capacity for a full invasion and occupation of Iran (ultimately necessary to guarantee regime change and fully destroy Iranian missile and drone capacity). Upping the intensity of bombing and lifting it to the strategic sphere would do more damage but achieve nothing new. A limited invasion would solve nothing and risk large numbers of casualties and an eventual retreat. So what to do? What’s left? A blockade! It is low risk (except to the world economy) and it looks like action.

There are other possible explanations. It could be that President Trump is preparing to accept a deal that is obviously a big win for Iran. Whatever one thinks of Donald Trump, he is a cunning media operator and brilliant salesman. Perhaps he could say that the few paltry concessions Iran offered were due to his blockade forcing them to back down from their maximalist position?

Or, it could be to prevent Western nations from breaking with Washington and giving the group of states doing deals with Tehran a critical mass. South Korea, Japan, and even Germany, were certainly looking as though they might be willing to play ball on Strait of Hormuz tolls. At that stage, the bandwaggoning impetus might have become irresistible. Not so fast, says Mr Trump! Now, nobody gets in or out.

Or, it might just be a dumb idea that will marginally hasten the world’s journey into economic depression and social unrest, and risks opening another front — against China no less! — when the US cannot even defeat Iran. You choose.

Until the Clouds Roll in a Little…

Folks, Producer Gav tells me that a couple of people subscribed to this Substack a week or so ago expecting to get the premium podcast episodes. It is true we do a premium podcast episode once a month, but that has hitherto been on Patreon only, which you can get for $8 a month. The last thing we want, though, is confusion. Therefore, those folks who subscribed here thinking they were getting the premium podcast have been refunded. To stop such confusion in future, we will put premium podcasts on here, too.

That stops the confusion, but it does mean we have to raise prices to cover the extra product. We have big plans for this Substack. It is going to be more — much more! — than this Brief. I think it is going to become much more than any of the geopolitical and geoeconomics Substacks out there. I am excited; Philip is buzzing. But in the meantime we are going to have to bring forward the price increase so that premium podcast episodes can be made available here and nobody feels let down.

So, from this week, or next at the latest, this Substack will be $12 (that works out as the same $8 that the Patreon guys pay, plus $4 for the written content, which makes me feel rather undervalued, but seems like a decent compromise). Shortly, we will start paywalling some articles. But you’ll get premium podcast episodes, this weekly Brief, and by the end of May, you’ll start getting so, so, so much more. I wanted to make all this clear, because I hate the idea of confusion whereby people end up feeling let down by us. I have also recorded a message about this matter for the podcast, too.

If you really cannot afford the equivalent of two pints over a whole to subscribe, please consider sharing this Brief with somebody who would benefit from reading it. It only takes about 30 seconds to do that, and we would very much appreciate it. Thank you in advance.

Multipolarity Brief will return next Tuesday. Until then, farewell and good luck.