Multipolarity Brief: Issue 16 — Iran Special XI

Do nothing. Win.; Driving season; If the mountain won't come to Muhammad…

Do nothing. Win.

The first evidence is arriving that Multipolarity Brief was correct to argue that China was far more resilient to the Hormuz Shock than Trump supporters often suggest. Two weeks ago, we detailed the seven points that led us to this conclusion. Briefly, they are: first, that China has diversified its imports away from the Strait, with only some 42% of its imports coming from the Gulf. Second, that China is a net exporter of refined products, and that by restricting exports, it could reduce the crude it needed to import. Third, that China has enormous stockpiles of crude: enough to last into autumn even if all oil had been cut off from the Gulf from the beginning of the conflict (which we know it wasn’t for China) and even if it failed to get replacement oil from elsewhere (which we know it can). In real terms, this means it could last well into next year, even without reordering its internal energy structure (unlikely) and even without demand destruction elsewhere in the world (already happening).

Fourth, that China has gigantic currency reserves, which would allow it to hoover up spare oil at whatever price for years. Fifth, that China is a leader in renewables and coal, giving it great flexibility in terms of re-ordering its internal energy structure. Sixth, that China’s economy is in a low-flationary or deflationary state, which affords its central bank more monetary policy room to mitigate the supply shock than western central banks, where inflation is a real issue. Seventh, that while China is no longer a Marxist-Maoist economy, the Communist Party has more command control over the levers of economic power than do western governments.

Now, the first evidence has arrived to support this thesis. Javier Blas, Bloomberg’s energy analyst, reports that China is significantly reducing its oil imports. He writes:

Over recent weeks, industry executives have noticed something odd: Chinese state-owned oil companies have been reselling some of their oil cargoes to European and Asian rivals. The behavior suggests surpluses — odd during a supply shortage.

[…]

Tanker-tracking data gives the same anomalous surplus signal. Vortexa, a commodity intelligence firm, estimates that China is buying just 8.2 million barrels a day of crude from overseas, down from a prewar level of around 11.7 million. The 3.5-million barrels a day swing almost matches the total consumption of Japan and is double the amount supplied by the United Arab Emirates pipeline that circumvents Hormuz

[…]

The import drop might make sense if Chinese commercial inventories were falling sharply, or if Beijing had tapped its strategic petroleum reserves. But neither is happening. Instead, commercial stockpiles have continued to increase in recent weeks, according to satellite data. What Beijing did was ban exports of refined products, effectively allowing refineries to process less crude to meet domestic demand. But the policy has now been reversed, suggesting the country sees enough fuel availability.

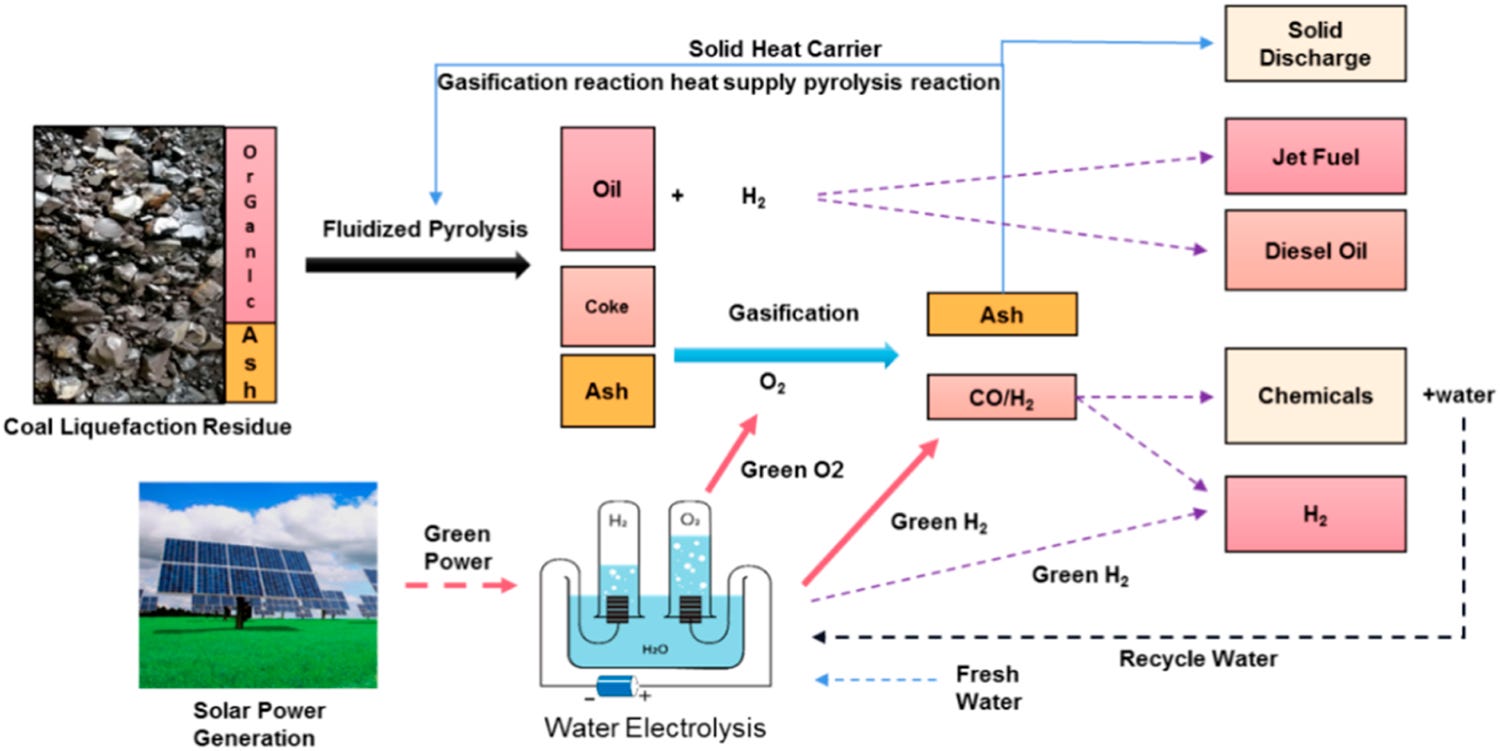

How is China doing this? Mr Blas crunches the numbers and rules out demand destruction. Instead, he suggests that China’s coal-to-petrochemicals industry is ramping up. This technology replaces crude oil with coal as the feedstock for plastics such as polyethylene, polypropylene and polyvinyl chloride. Mr Blas finds that these plants have been “have been running hard for the last 60 days, in turn reducing consumption of traditional feedstocks such as ethane and naphtha.”

A flow chart of the coal to liquids industrial process.

Funny that, because two weeks ago, in our aforementioned Brief, we wrote that China “has also invested in coal-to-liquids/chemicals technology that could be rushed ahead.”

Whatever the reason, the fact remains that heavily reducing imports is not the behaviour of a country that believes it is likely to struggle to stay afloat amid an oil shock. Indeed, Javier Blas reveals that China has ended many export controls on refined products and is actually reselling some crude to rivals in Europe and East Asia, suggesting it has a surplus. So much for the 17-D Chess argument that losing a war against Iran was actually a win because it would hobble China’s economy. It is long past time to dismiss these arguments, and those peddling them, as unserious.

Our keenest readers will also remember, though, that in the same dispatch we shared translations of the papers and columns economic analysts from China had written, which argued that the Iran War might improve China’s relative economic competitiveness vis-à-vis its rivals in Asia and Europe. One specific example we noted in our Brief two weeks ago was EVs. China has developed an electric vehicle industry so powerful that rival nations — especially in Europe and North America — have complained bitterly that China’s ‘overproduction’ of EVs would destroy their own car industry. An oil shock is only likely to increase demand for these cars, and China sure as heck has the capacity to fulfil such demand, we argued.

And lo! This week, the Wall Street Journal reports fresh data which supports our expectations. China’s export “of new-energy vehicles more-than doubled to 406,000 units in April, the data showed,” the Journal writes. This trend will only continue was Western petroleum reserves reach the bottom of the barrel and the supply shock really starts to bite. From the consumer perspective, internal combustion engine cars will seem an ever-worse offering compared with EVs, and China is already the market leader, and probably the only player able to rapidly fill any sudden rise in demand for EVs. Meantime, from a governmental perspective, diversification away from these supply risks will become a more urgent matter. China also dominates the market for solar panels and battery storage, and is a leading player in wind-based electricity generation.

So much for owing the Chinese.

Driving season

Meanwhile, as the war continues, three pressures are building on the Trump Administration: internal political pressure, global macroeconomic pressure, and pressure from front-line allies.

We hardly need to be reminded that this is a midterm election year. Nor do we need to be reminded what a big Democrat victory would likely do to President Trump’s ability to govern. In addition to probably being obstructionist — playing games to set the table for the next presidential election — a Democrat controlled Congress would likely seek to entangle the US President in a thicket of impeachment and other legal bocage. The stakes, therefore, are even higher than they usually would be at a midterm election.

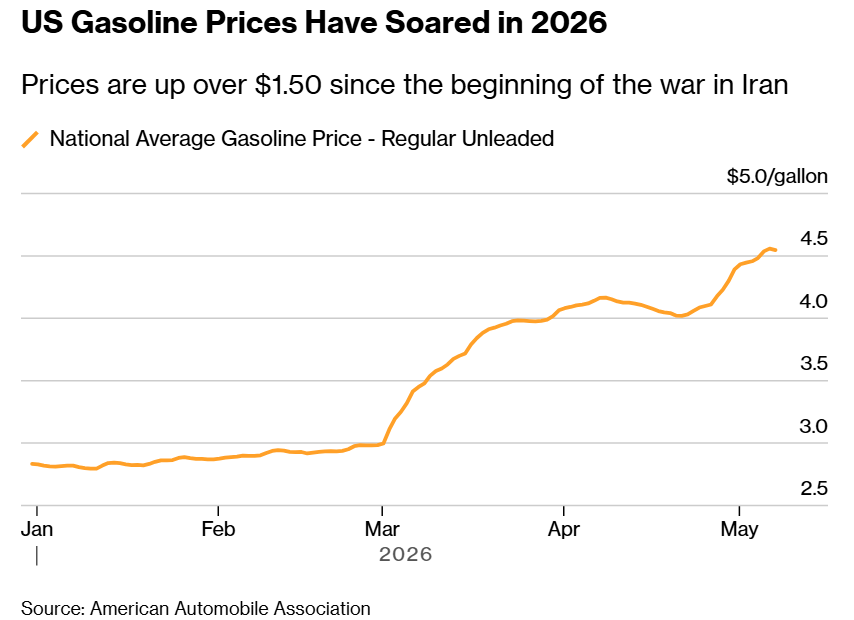

And in an extremely bad sign of Republican electoral prospects, the analysts at JP Morgan Chase have argued that $5-a-gallon gasoline prices at the pump are coming into view.

From Bloomberg: Gasoline prices are already 50% up since the beginning of the war.

“If refinery runs continue to be constrained by limited supplies of crude, fuel prices, rather than crude prices, may become the ‘primary transmission channel for demand destruction,’” the JP Morgan analysts wrote. “In that scenario, crude could plausibly stabilize around $100 even as product cracks widen sharply. The next phase of the shock then may look less like a classic crude spike and more like a refining and end-user fuel crunch.”

It should be noted here that ‘demand destruction’ is economistese for ‘factories shutting down, people driving their cars less, and consumers buying less stuff that has to be transported to shops or made from things with petrochemical feedstocks (like plastics or clothes)’. Demand destruction, though, in addition to being more concise, doesn’t quite bring to mind the economic hardship that is its reality on Main Street. Yet this is ultimately the way in which commodities markets, like oil, find balance during supply shocks. (See: The Three Day Week in 1970s Britain.)

Since the beginning of the war, Americans have already spent an additional $23.9 billion more on gasoline than they did over the same period last year. And driving season is coming into view just as the oil shock starts moving down the pipe into refining. Memorial Day (this year on 25 May) marks the beginning of the period in which Americans traditionally do far more driving (for vacations and the end of university years and similar). It lasts until Labour Day in early September, peaking in July and August. Great timing for an oil shock!

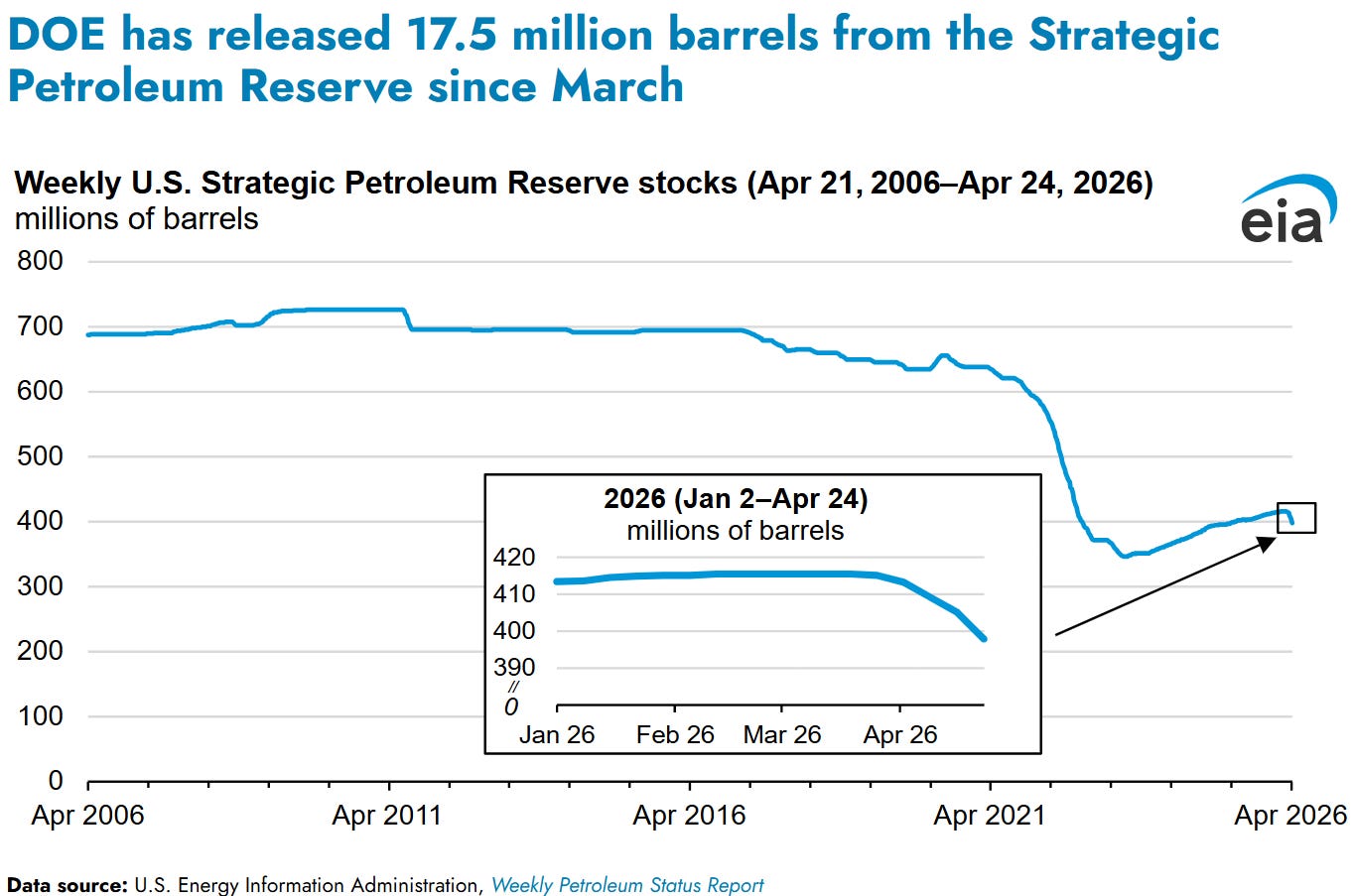

Recall that on 31 March 2022, then-President Joseph Biden, ordered an unprecedented release from the US Strategic Petroleum Reserves to mitigate the energy market shock caused by the Russian invasion of Ukraine. 2022 was a midterm year, too, and there was little doubt about the political motivation for this release. Yet the reserves have hardly been refilled since, despite much lower oil prices. They are now being emptied again. The problem President Trump faces is that they cannot go to zero without structurally damaging the salt caverns in which they are held.

A Wall Street Journal report suggests President Trump’s advisors are well aware of this risk — and sufficiently concerned to use the media to sound the alarm. Political pressure is not a theoretical risk, but a concrete and increasing restraint on action. We note that there is a very real possibility that this situation leads to the imposition of export controls, which would be devastating for the rest of the world.

In addition, the US faces a second pressure. As bad as the economic hit on the US will be, it will be far worse on Europe and on US allies in the Asia Pacific region like Japan and Australia. As the economic effects mount, so will diplomatic pressure on the Trump Administration to bring the war to a close. The final pressure will come from front line states, sans-Israel. Kuwait, Saudi Arabia, Bahrain, Qatar, and the UAE all face increasing economic strains and are suffering accumulating infrastructure damage. The entire economic model of the UAE might be at risk, if expats no longer see it as a safe place to do business and trade.

Increasingly, these nations will raise the pressure, such as they can, on the US to end the mess on whatever terms it can get — and will likely look for ways to help that process along. We already saw a hint of this in action as President Trump was forced to U-Turn on his plan to open the Strait of Hormuz after Saudi Arabia temporarily suspended the rights of the US Air Force to use Saudi bases and airspace to attack Iran.

Far from outlasting China, it is the US that faces increasing pressure — political and diplomatic. Furthermore, if the Multipolarity Brief can see this, then the Iranians sure as heck can. Given their far greater pain tolerance, they have every incentive to wait out the US to secure the best possible deal.

The problem is that, as we have said since the second week of the war, no viable landing space exists for a deal. Iran’s bottom line would be politically unacceptable in Washington, and the present American offer is nowhere near what Tehran could ever accept to call a halt to the impasse.

If the mountain won't come to Muhammad…

The risk is that US allies decide that their only option is to go to the mountain, so to speak, and do bilateral deals with Tehran to get the oil, fertilizers, naptha, sulphur and the rest of the things they need out of the Gulf (or, from the Gulf state perspective, to take those political and diplomatic steps needed for Tehran to remove them from the IRGC crosshairs): to essentially accept Tehran’s terms.

In this scenario, the war does not end with a peace deal, but with a series of bilateral agreements to get the oil flowing. Washington would be sidelined, as states quietly agreed to accede to Iranian demands (those nations with frozen assets would have to return them, and tolls for passage through the Strait paid) while frontline states asked the US to leave its bases and refused to allow the USAF to overfly their nations on the way to Iran. Of course, the US could contest such moves. It could sanction those ships dealing with Iran. It could impose secondary sanctions on countries and companies who repatriated frozen assets or paid tolls. It could fly over Saudi Arabia or Kuwait anyway, and challenge them to shoot at the USAF.

What an ungodly mess.

Yet there is another risk. This is that President Trump travels to Beijing this week and asks them to help him to cut the Godian Knot. In fact, two months ago, Multipolarity Podcast co-host Philip Pilkington forecasted that this was exactly how the war would end. He argued that Trump would be forced to go to China to ask it to use its leverage with Tehran to bail out the US. Xi’s likely asking price, per Mr Pilkington? Taiwan.

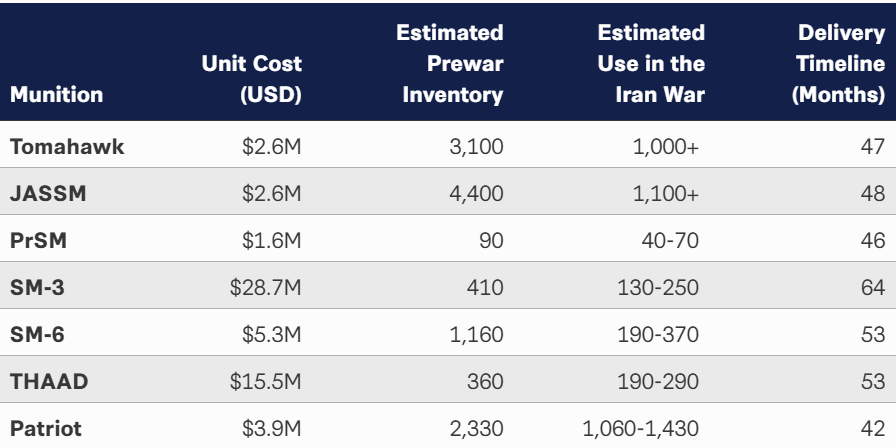

This kind of bargain — once unthinkable in Washington — might appear appealing in the present strategic environment. The Centre for Strategic and International Studies (not a think tank prone pacifism) pointed out in an April paper that the US had fired more than 50% of its available munitions in some catagories.

"In the 39 days of the air and missile campaign before the ceasefire, U.S. forces heavily used the seven munitions in Table 1 [below]. For four of them, the United States may have expended more than half of the prewar inventory. Rebuilding to prewar levels for the seven munitions will take from one to four years as missiles in the pipeline are delivered.”

Source: CSIS

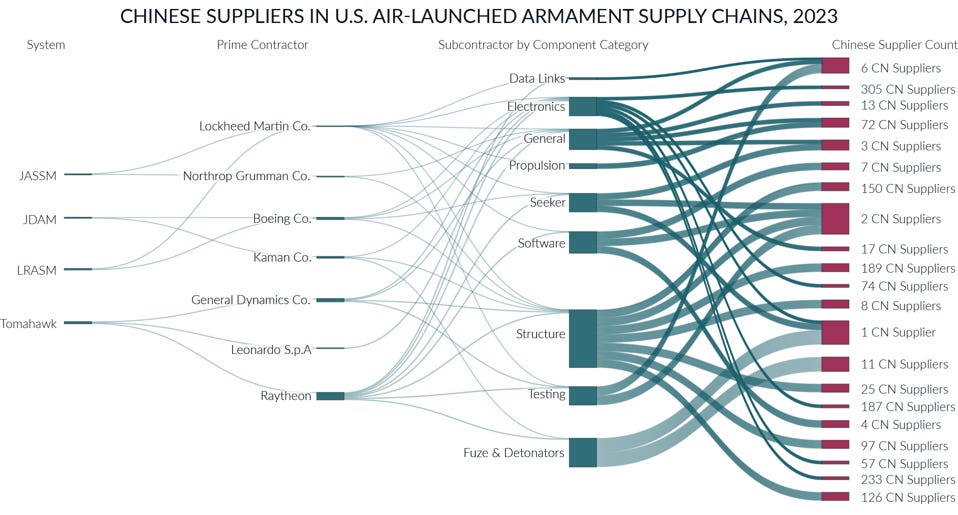

We would add that the replenishment of stocks “to prewar levels for the seven munitions will take from one to four years” if China permits it. The chart below shows the extent to which Chinese suppliers are crucial to the US weapons manufacturing process.

Source: Forbes

Furthermore, China has a chokehold on the supply of refined rare earths, which are vital for the production of said weapons.

As CSIS argues, it is not fighting the Iran war that the US must be immediately concerned about, but what is left to fight future wars. “Even before the Iran War,” it writes, “stockpiles were deemed insufficient for a peer competitor fight. That shortfall is now even more acute, and building stockpiles to levels adequate for a war with China will take additional time."

When thinking about US magazine depletion, we might also add on the ATGMs, ATACMS HIMARS, MANPADS, and Patriots sent to Ukraine to fight Russia in another peripheral theatre.

Yet the Iran War has revealed that the US might not be able to defend Taiwan even if it had a full magazine. Friend of Multipolarity Anusar Farooqui, the hedge fund CEO and one-time geopolitical scholar who runs the Policy Tensor Substack, has produced an arresting paper which suggests that the US has no ability to win a war against China in the Western Pacific. He constructs a model using known data on missile intercept rates and circular error probability accuracy that shows US bases in the Western Pacific are not survivable in a war with China. Without these bases, the US would not be able to defend Taiwan.

In this environment, it might seem to the US that, if it could get some kind of favourable trade agreement with China and a solution to Iran, sacrificing a pawn that it can anyway no longer reasonably be expected to defend would be a good deal.

And with Taiwan goes the Philippines, and probably South Korea. Japan becomes harder to defend. Après Trump, le deluge.

Of course, the very weakness of the US suggests it would seek to avoid any grand bargains, but there is little doubt that Washington will at least attempt to feel out a Chinese asking price for helping with Iran.

Until the Clouds Roll in a Little…

Did you think the effort we put into researching and writing this dispatch brought you some value? Then take 10 seconds to subscribe for free right now. From next week, far more articles will begin appearing on this Substack. We are tremendously excited. If you want, you can get ahead of that with a paid sub right now. As part of that deal, you would also get access to our premium podcast episodes. Pretty, pretty good.

If you truly cannot spare the price of two pints of beer in a pub for a whole month’s content, would you do us a favour? Could you take just one minute of your time to share this with somebody who would benefit from reading it? Or maybe announce on social media how much you enjoyed it. We’d appreciated it greatly, and it helps a lot. Thank you in advance. Oh, and one more thing: do comment below. Don’t be scared. I’ll reply to questions.

Multipolarity Brief will return next Tuesday. Until then, farewell and good luck.

A summary that leaves a slight sense of relief.

Much needed right about now.